How To Calculate House Payment: A Comprehensive Guide

Understanding how to calculate house payment is crucial for anyone looking to buy a home. Whether you're a first-time homebuyer or an experienced homeowner, knowing how to accurately calculate your monthly mortgage payments can save you money and help you make informed financial decisions. In this article, we will explore the various components that make up a house payment, how to calculate it step-by-step, and tips for managing your mortgage effectively.

Many potential homeowners often underestimate the total costs associated with homeownership. It's not just about the mortgage payment; there are property taxes, insurance, and maintenance costs to consider. By the end of this article, you will have a clear understanding of how to calculate house payment and what factors influence it.

Additionally, we will provide you with valuable resources and tools to assist you in your home-buying journey. Armed with this knowledge, you can confidently approach your home purchase, ensuring that you choose a mortgage that fits your budget and lifestyle.

Table of Contents

- Components of a House Payment

- How to Calculate House Payment

- Understanding Amortization

- Additional Costs to Consider

- Types of Mortgages

- Tips for Managing Your Mortgage

- Common Mistakes to Avoid

- Useful Resources

Components of a House Payment

When calculating your house payment, it is essential to understand the various components that contribute to the total amount you will pay each month. These components include:

- Principal: The amount of money you borrow to purchase the home.

- Interest: The cost of borrowing the principal amount, expressed as a percentage.

- Property Taxes: Local government taxes based on the assessed value of your property.

- Homeowners Insurance: Insurance that protects your home and possessions from damage or loss.

- Private Mortgage Insurance (PMI): Insurance required if your down payment is less than 20% of the home's value.

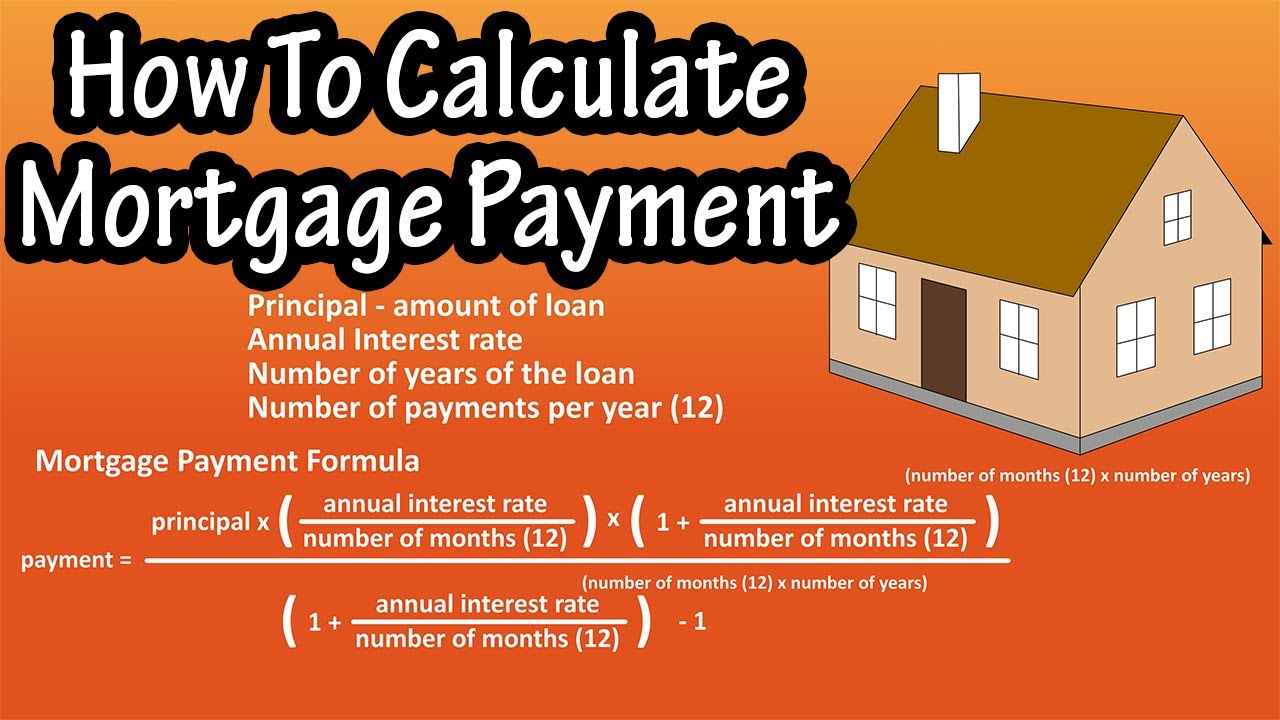

How to Calculate House Payment

Calculating your house payment involves a simple formula. Here’s how to do it step-by-step:

- Determine Your Loan Amount: This is the purchase price of the home minus your down payment.

- Find Your Interest Rate: This is the annual interest rate offered by your lender.

- Choose Your Loan Term: Common terms are 15 or 30 years.

- Use the Formula: The formula to calculate your monthly mortgage payment (M) is:

M = P[r(1 + r)^n] / [(1 + r)^n – 1]

Where:

P = principal loan amount

r = monthly interest rate (annual rate divided by 12)

n = number of payments (loan term in months)

Example Calculation

Let’s say you want to buy a house for $300,000 with a 20% down payment and a 4% interest rate on a 30-year mortgage.

- Down Payment: $60,000 (20% of $300,000)

- Loan Amount: $240,000 ($300,000 - $60,000)

- Monthly Interest Rate: 0.00333 (4% annual rate ÷ 12)

- Number of Payments: 360 (30 years x 12 months)

Using the formula above, the monthly payment would be approximately $1,145.80.

Understanding Amortization

Amortization is the process of spreading out a loan into a series of fixed payments over time. Each payment covers both principal and interest, and the breakdown changes as the loan matures.

- In the early years, a larger portion of your payment goes towards interest.

- As time goes on, more of your payment will go towards paying down the principal.

This gradual shift can have significant implications for your overall interest payments over the life of the loan.

Additional Costs to Consider

When calculating your house payment, it's essential to factor in additional costs that can significantly impact your budget:

- Property Taxes: These can vary significantly based on your location and should be included in your monthly calculations.

- Homeowners Insurance: This is typically required by lenders and protects your investment.

- PMI: If applicable, this insurance can add a considerable amount to your monthly payment.

- Maintenance and Repairs: Setting aside funds for unexpected repairs is crucial for long-term financial health.

Types of Mortgages

Understanding the different types of mortgages available can help you choose the right one for your financial situation:

- Fixed-Rate Mortgage: Offers a stable interest rate and monthly payment over the life of the loan.

- Adjustable-Rate Mortgage (ARM): Features a lower initial interest rate that can change after a specified period.

- Government-Backed Loans: Include FHA, VA, and USDA loans, which may offer lower down payment options.

Tips for Managing Your Mortgage

Once you have your mortgage, managing it effectively is key to maintaining financial stability. Here are some tips:

- Set a Budget: Ensure your total housing costs fit within your budget to avoid financial strain.

- Make Extra Payments: If possible, make additional payments towards the principal to reduce interest costs.

- Refinance: Consider refinancing if interest rates drop significantly to lower your monthly payment.

Common Mistakes to Avoid

Avoiding common pitfalls can save you time, money, and stress:

- Not Shopping Around: Failing to compare mortgage offers can lead to missed savings.

- Ignoring Other Costs: Focusing only on the mortgage payment without considering additional costs can lead to budget issues.

- Underestimating Your Budget: Make sure to account for lifestyle changes and potential emergencies.

Useful Resources

To assist you in your home-buying journey, consider using the following resources:

- Bankrate Mortgage Calculator

- U.S. Department of Housing and Urban Development (HUD)

- Consumer Financial Protection Bureau (CFPB)

Conclusion

In conclusion, knowing how to calculate house payment is essential for any prospective homeowner. By understanding the components of your payment, utilizing the correct calculations, and being aware of additional costs, you can make more informed decisions about your mortgage. Ensure to consider different mortgage options and manage your payments wisely to protect your financial future.

We encourage you to leave a comment below if you have any questions or share this article with someone who might find it useful. Additionally, check out other articles on our site for more helpful tips!

Penutup

Thank you for reading! We hope you found this guide on calculating house payments informative and valuable. Remember, knowledge is power, especially when it comes to making one of the most significant financial decisions of your life. We look forward to seeing you again on our site for more tips and insights!

Understanding WS Stock: A Comprehensive Guide To Wealth Creation

Fidelity Blue Chip Growth: A Comprehensive Guide To Investment Success

AFCON 2024 Schedule: Everything You Need To Know

{kind=link}